The program of the Bangko Sentral ng Pilipinas’ to encourage the use of digital payment platforms got a boost during the ongoing enhanced community quarantine (ECQ) across the country due to the COVID-19 pandemic. The BSP has urged the public to utilize e-payment platforms to help address the rise of the virus and lessen the transmission.

The BSP has initially set an ambitious target to increase the value and volume of e-payment transactions to reach 30% and 20% of the total respectively by 2020.

According to the central bank, transactions from several platforms such as PESONet and InstaPay, real-time electronic payment systems under the National Retail Payment System (NRPS), have been visibly increased since people are restricted to move outside of their houses.

The value of PESONet transactions before the ECQ was recorded at around PHP6 billion daily and currently has surpassed PHP 6 billion in most days from March 17 until April 2, 2020. Data obtained from the central bank also showed that the value of InstaPay transactions is also generally higher during the ECQ.

Consequently, both the cheque payments and automated teller machines (ATMs) withdrawals declined during this time. Cheques which are largely used by business entities significantly declined in volume and value because of lower business transactions during the ECQ. The value of daily cheque transactions averaged at about PHP50 billion to PHP 75 billion from March 17 until April 2, 2020, from the previous PHP 150 billion daily.

Meanwhile, the unfavorable effect of work suspension on millions of workers across the country is reflected in the downtrend of ATM withdrawals. The minimum daily value of ATM withdrawals was recorded at about PHP 3 billion from March 2 until March 16, 2020, with the highest at approximately PHP 9 billion. The daily transactions from March 17 to April 2 was recorded at about PHP 3 billion to PHP 4 billion, with the highest at PHP 5 billion.

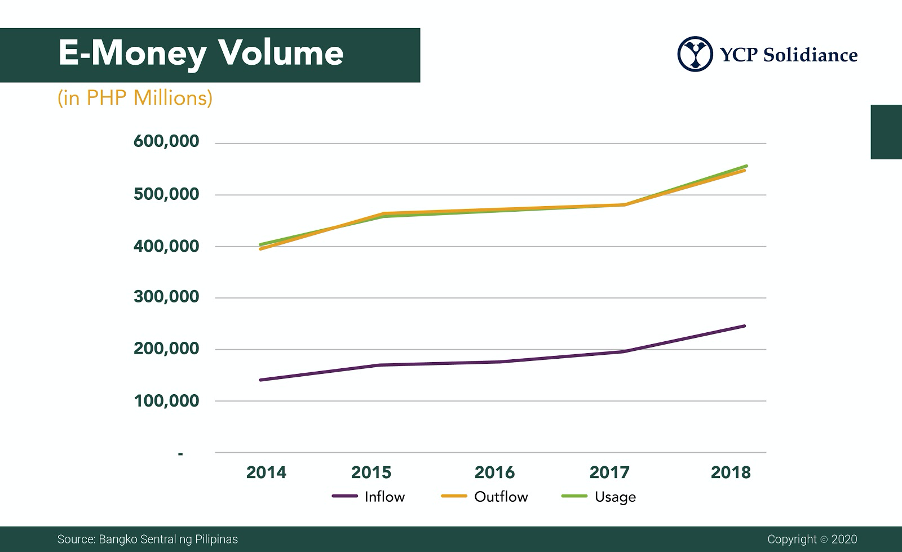

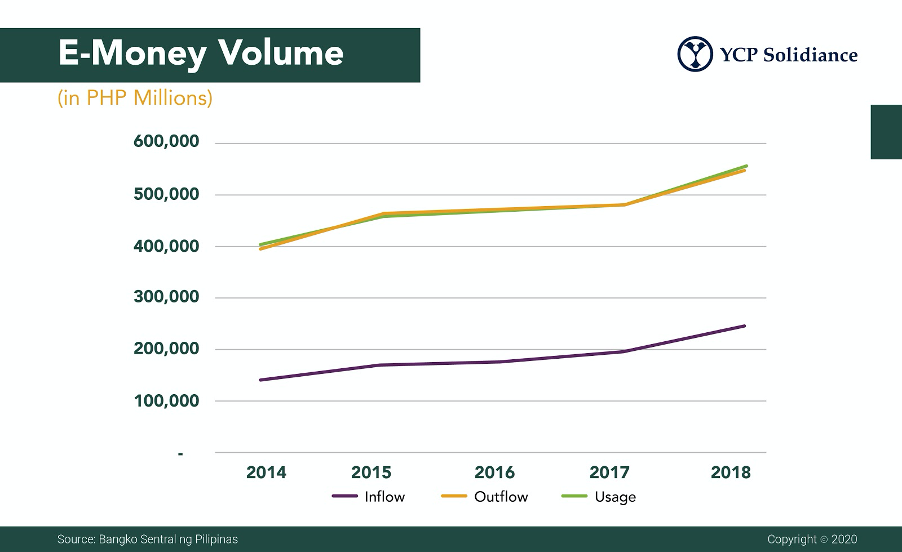

Presently, E-money remains a very small segment of the country’s transactions, but its historical growth is indicative of the very high potential it has to change the payment landscape in the Philippines. According to the latest YCP Solidiance’s report, “The Digitization of the Philippine Wallet: E-Money’s Emergence in the Philippines”, 99% of payments in the country are still made in cash despite the availability of e-money.

Having acknowledged the invaluable role of e-money in the path to financial inclusion for a largely underbanked population, both the central bank and private companies have been promoting its use and innovation.

This has led to substantial growth for e-money over the past few years. E-money has seen a steady growth from 2014-2018, with an 8% compound annual growth rate (CAGR) in amount inflows and even 15% for amount usage. Transaction numbers are also seeing steep growth rates across e-money inflow, outflow, and usage, with usage boasting a 36% CAGR from 2014-2018, indicating that e-money is definitely being used more frequently across the years

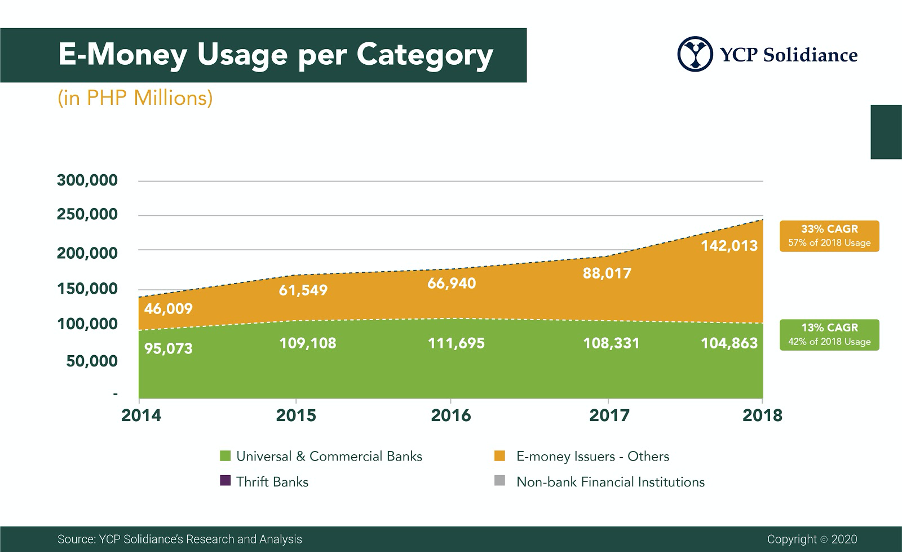

The report recorded that e-money’s size and growth is largely driven by the banking segment in terms of inflows and outflows. With regard to usage, E-money Issuers, which is comprised of the mobile wallet companies, lead other categories. Mobile wallets’ usage growth rates have overtaken the banks’ in 2018, indicating its growing significance in the industry and their capabilities in influencing the spending behaviors of the Filipinos.

Leading the Charge: Major Players in SEA’s Digital Lending Market

The fintech lending market in SEA is poised for substantial growth, including digital lending which is set to surpass digital payments as the primary revenue driver for the region's digital financial services sector by 2025, with a compound annual growth rate (CAGR) of 33%. This growth is fueled by the widespread adoption of automated loan origination processes and the seamless integration of financial services into digital platforms.

Unlocking Opportunities in the SEA Digital Financial Services Landscape

In recent years, Southeast Asia (SEA) has emerged as a hotbed for fintech innovation, transforming the financial landscape across its diverse markets. This transformation is characterized by a surge in digital financial services (DFS), revolutionizing how individuals and businesses manage their finances. However, the journey is not without its challenges, and understanding these is crucial for stakeholders aiming to navigate this rapidly evolving sector.

How SEA Startups are Navigating Funding Challenges

The startup ecosystem in Southeast Asia (SEA) has long been a vibrant hub for innovation and growth. However, recent global economic shifts and the aftermath of the COVID-19 pandemic have ushered in a new era of funding challenges.

Challenges for Sustainable Recovery in Southeast Asia

Sustainable recovery in Southeast Asia faces numerous challenges, yet also presents significant opportunities for green growth. Addressing sustainable issues is crucial for achieving a resilient and sustainable future.